Call us today!: (440) 610-2804

Summary:

When filing a roof insurance claim, understanding the difference between Actual Cash Value (ACV) and Replacement Cost Value (RCV) can significantly impact how much you receive. This guide explains both terms in simple language so Ohio homeowners know what to expect before starting a claim.

Why Understanding Your Policy Matters

After a storm, most homeowners focus on damage—but not their policy.

That’s where confusion begins.

Insurance companies don’t all pay claims the same way, and the type of coverage you have directly affects your payout.

If you’re new to the claims process, start with our guide on

how roof insurance claims work (step-by-step guide for Ohio homeowners) (internal link).

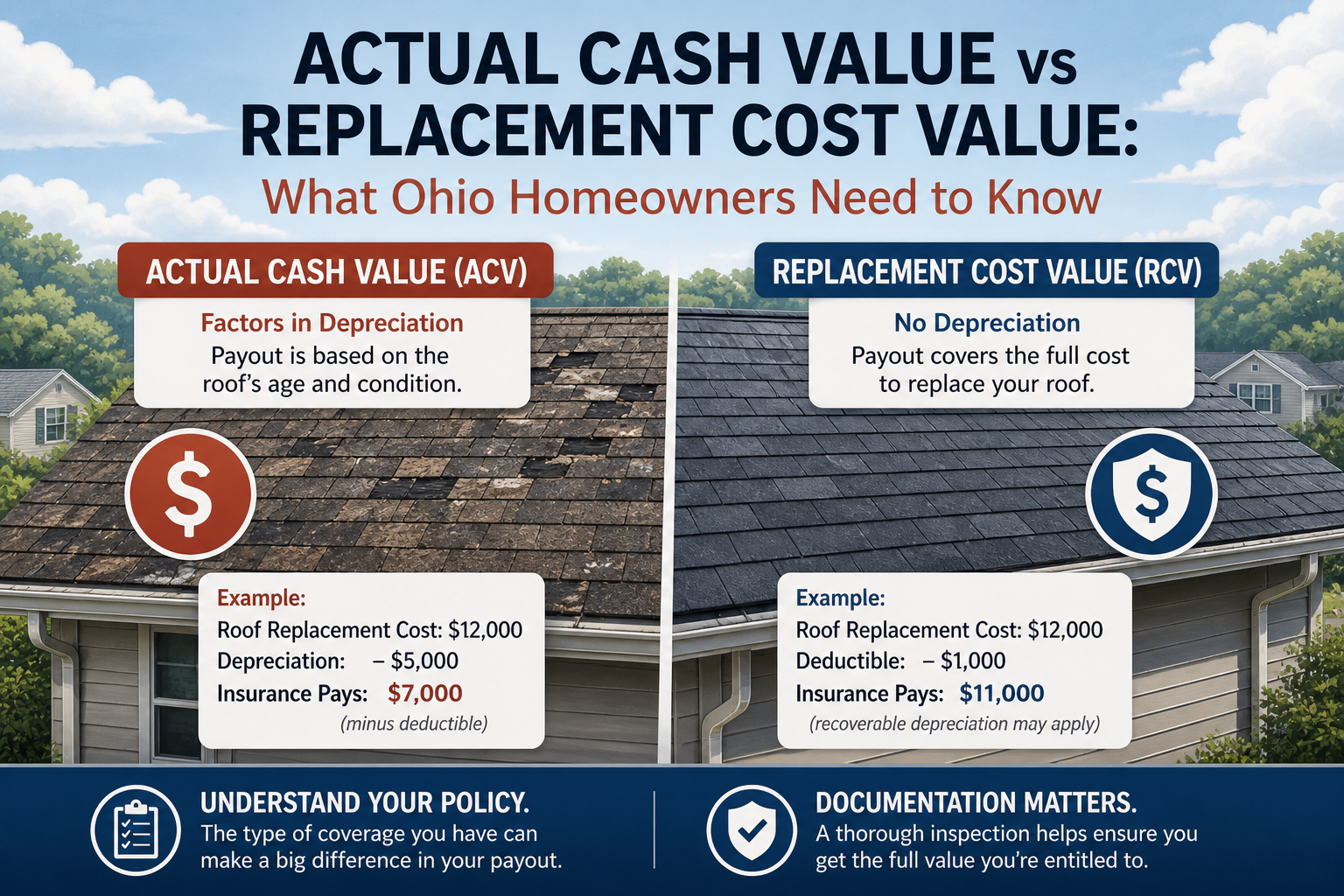

What Is Replacement Cost Value (RCV)?

Replacement Cost Value means your insurance covers the full cost to replace your roof (minus your deductible).

Example:

- Roof replacement cost: $12,000

- Deductible: $1,000

- Insurance pays: $11,000

However, most policies:

- Pay part upfront

- Hold back depreciation until the job is completed

This is called recoverable depreciation.

What Is Actual Cash Value (ACV)?

Actual Cash Value accounts for depreciation based on age and condition.

Example:

- Roof replacement cost: $12,000

- Depreciation: $5,000

- Insurance pays: $7,000

That means you’re responsible for the difference.

Why This Difference Matters

The gap between ACV and RCV can be thousands of dollars.

Many homeowners don’t realize:

- Older roofs are often depreciated heavily

- ACV policies shift more cost to the homeowner

- Documentation plays a major role in claim outcomes

How Roof Condition Affects Your Claim

Insurance companies evaluate:

- Age of the roof

- Material type

- Existing wear and tear

- Storm-related vs pre-existing damage

This is why inspections matter.

If you haven’t already, review

what a free roof inspection should actually include (internal link)

to understand how damage is properly documented.

Where Drone Inspections Help

High-resolution documentation can strengthen your claim.

Drone inspections allow contractors to:

- Capture clear damage evidence

- Identify impact points

- Provide visual support for adjusters

This ties directly into our article on

why drone roof inspections are safer for your home (internal link).

Common Mistakes Homeowners Make

- Filing a claim without documentation

- Not understanding their policy type

- Waiting too long after a storm

- Assuming all damage will be covered

These mistakes can reduce or delay payouts.

When to Get a Professional Opinion

Before filing a claim, it’s often best to:

- Have your roof inspected

- Understand the extent of damage

- Review whether a claim makes sense

Working with a local company like Jarrell Roofing ensures you get a clear, honest assessment.

Final Thoughts

Understanding ACV vs RCV gives you control over the claims process.

Knowing what your policy covers—and what it doesn’t—helps you avoid surprises and make informed decisions after a storm.

Not Sure What Your Policy Covers?

Jarrell Roofing offers free inspections with full documentation, helping homeowners determine whether filing a claim makes sense before contacting insurance.

📞 Schedule your inspection today and get clarity before taking the next step.